Christian, a barista at Lucky Goat Coffee House in Brewerytown, swipes a credit card through their Square register. Credit: Sam Newhouse

Christian, a barista at Lucky Goat Coffee House in Brewerytown, swipes a credit card through their Square register. Credit: Sam Newhouse

All around Philly, small shops that used to be cash-only are now accepting cards, thanks to the increasing ubiquity of Square — a small white credit card reader that can attach to cell phones or iPads.

“The traditional route of accepting credit cards or advancing capital has a lot of unknowns, that are quite punitive in the long run,” said Square CEO Jack Dorsey, 37, who also co-founded Twitter, and was in Philadelphia Tuesday to participate in a panel discussion at UPenn.

“We saw sellers miss sales because they couldn’t accept credit cards,” Dorsey said. “So we put out a free reader, we made the cost 2.75 percent for every swipe, then we advance people the capital from that card swipe the next business morning … It’s making sure our sellers could accept every payment that comes across the counter.”

“It wasn’t just about shaving pennies. It was really about providing predictability … That helped us build our network,” he said.

Launched in 2010, Square has now spread to the point where all Square-using merchants are collectively the 13th largest retailer in the country, just under giants Best Buy and McDonald’s.

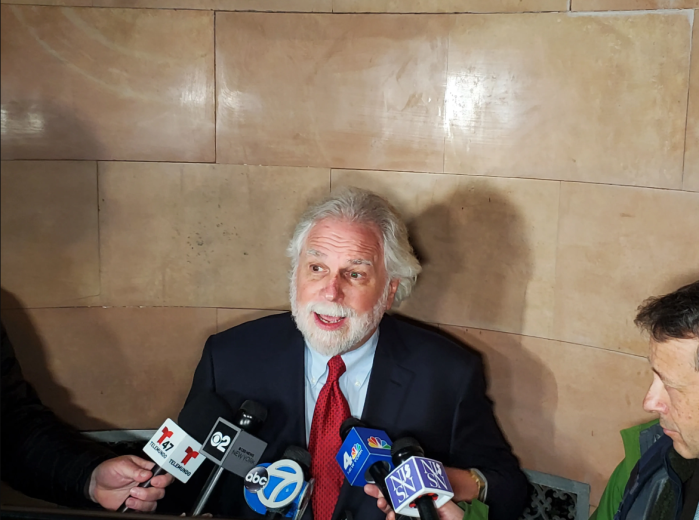

Drew Crockett, owner of Hubbub Coffee and a merchant who uses Square, left, with Square CEO Jack Dorsey. Credit: Sam Newhouse

Drew Crockett, owner of Hubbub Coffee and a merchant who uses Square, left, with Square CEO Jack Dorsey. Credit: Sam Newhouse

Here in Philadelphia, three of the five Green Line Café locations use Square, said co-owner Daniel Thut.

About a third of our customers use credit cards, and accepting cards has increased sales about five to 10 percent, he said.

“One thing I like about Square is that I know exactly how much it’s going to cost me, there’s transparency in pricing that we didn’t experience with our previous credit card processor,” Thut said. “It does feel a little weird to think that two or three credit card companies get a small slice of so many economic transactions in this country. But there is a cost in dealing with cash that’s avoided with credit cards, so perhaps it can actually make the economy more efficient.”

Maddie Bird, left, and Emily Childs, right, baristas at Hubbub Coffee, in front of their Square register. Credit: Sam Newhouse

Maddie Bird, left, and Emily Childs, right, baristas at Hubbub Coffee, in front of their Square register. Credit: Sam Newhouse

Drew Crockett, owner of Hubbub Coffee, which began as a truck on UPenn’s campus, said he got a Square as soon as possible.

“When we started in a truck, one frustration of ours was not being able to accept cards. When the Square reader was introduced, we were a pretty early adopter of that – we just plugged it into my phone and were able to accept credit cards.”

Square started offering capital advances this year.

“We saw a lot of small businesses go try to get a loan from a bank. This is a process that can take anywhere form six months to a year,” Dorsey said. “That’s a lot of time wasted.”

With an advance from Square, Crockett invested in marketing — designing their trademark cups, which have to be bought in bulk, and getting the catering menu redesigned.

Square extends capital to merchants after analyzing data from that business’ sales, and with a tap on the email to accept, that business can receive the capital the next day.

There is no interest charged and no deadline to pay on Square Capital advances so the money is technically not the same as a loan.

The advance will come with an agreement to pay back a slightly larger amount, such as a $5,000 advance for a $5,500 repayment, or a $10,000 advance for an $11,000 repayment.